Who pays for title insurance in Texas, and what does each policy cover?

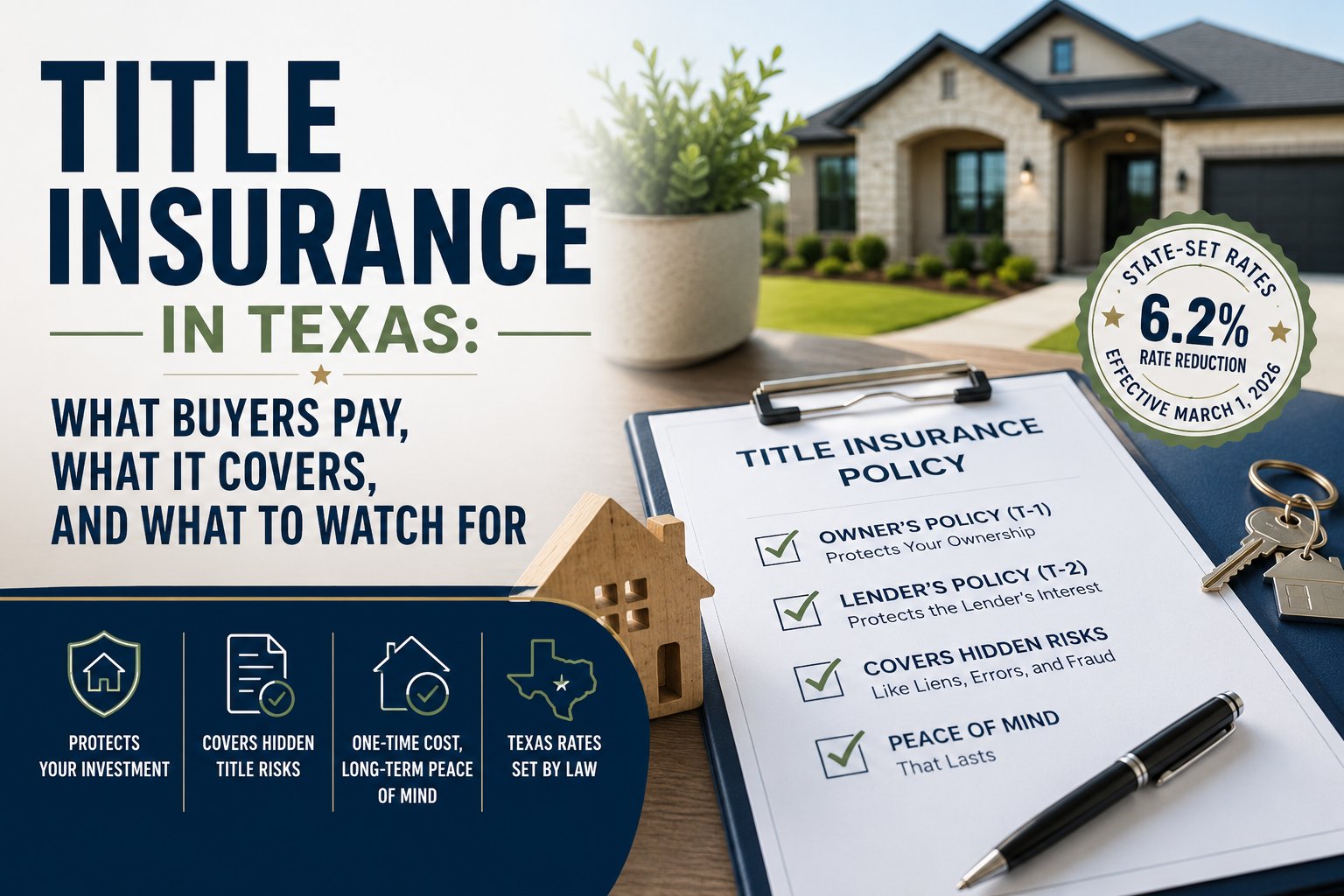

In Texas, buyers typically pay for the Lender's Policy (T-2), which protects their mortgage lender, while the seller pays for the Owner's Policy (T-1), which protects the buyer's ownership interest. Both are required at closing on any financed purchase. Texas title insurance premiums are set by the state — every title company charges the same rate — and the Texas Department of Insurance reduced those rates by 6.2% effective March 1, 2026. Buyers should review their title commitment's Schedule B exceptions before closing to understand what the policy won't cover.

By Cindy Dunnican | June 30, 2026

Title insurance is one of the most misunderstood line items on a Texas closing disclosure. Buyers see two separate charges — one for the owner's policy, one for the lender's policy — and they're not always sure what each one does, who's paying what, or whether they actually need both.

The short answer: yes, you need both. And in Texas, the way those costs are split is a little different from what buyers in other states might expect. Here's what you're actually paying for, what it protects, and what to review before you sit down at the title company table.

Two Policies, Two Purposes

Every financed Texas home purchase involves two separate title insurance policies. They cover different parties and serve different purposes.

Owner's Policy (T-1): This policy protects you — the buyer — against financial loss from title defects that existed before you purchased the property. It covers your ownership interest for as long as you or your heirs own the home. It's a one-time premium, paid at closing, that protects you indefinitely.

Lender's Policy (T-2): This policy protects your mortgage lender's lien position — not you. It's required by virtually every lender on a financed purchase. The coverage decreases as you pay down the loan and expires when the mortgage is paid off or refinanced.

Both policies protect against the same kinds of title defects. The difference is who receives the protection and how long it lasts.

What both policies cover:

- Unpaid liens from prior owners — contractor liens, HOA liens, tax liens, judgment liens

- Forged or fraudulent signatures on prior deeds

- Undisclosed heirs who claim a legal interest in the property

- Errors or omissions in public records

- Fraud or forgery in the chain of title

If any of these issues surface after you close, the title company defends you in court and pays for covered losses — up to the policy limit. For the Owner's Policy, that limit is the purchase price of the home.

Who Pays What — and Why It Works the Way It Does in Texas

Here's where Texas diverges from many other states: by custom across most North Texas counties — including Rockwall, Dallas, and Collin — the seller pays for the Owner's Policy (T-1) and the buyer pays for the Lender's Policy (T-2).

This surprises buyers who've purchased homes in other states, where buyers often pay for both policies. It surprises some sellers, too, who didn't realize they were footing the larger of the two premiums.

The reason this custom developed is straightforward: the seller is the one transferring a clear title to the buyer. Paying for the Owner's Policy is an extension of that obligation — a guarantee that the title they're delivering is insured against defects.

Both costs appear on the closing disclosure. The seller's Owner's Policy charge shows up in the seller's column. Your Lender's Policy charge shows up in your column — along with the settlement or escrow fee, which is the title company's charge for handling the closing itself.

A few things worth knowing:

- It's negotiable. The TREC contract specifies who pays each policy, and buyers and sellers can negotiate different arrangements. In a buyer-leaning market like North Texas in mid-2026 — where roughly 70% of Rockwall County homes are closing below list price — asking the seller to cover both policies as a concession isn't unreasonable.

- The seller typically chooses the title company. Because the seller is paying the larger premium, it's customary for the seller to select the title company in Texas. This is specified in Paragraph 6 of the TREC contract.

- Cash buyers still benefit from the Owner's Policy. If you're paying cash, there's no lender and therefore no Lender's Policy required. But a cash buyer who skips the Owner's Policy is accepting real risk — and most experienced buyers (and their agents) recommend it even when it's not legally required.

The 2026 Rate Change — What It Means for Your Closing

Texas title insurance premiums are promulgated — set by the Texas Department of Insurance and the same at every title company statewide. You can't find a lower T-1 or T-2 premium by shopping around. What you can compare between title companies is the settlement or escrow fee (typically $250–$750) and any endorsement or ancillary charges.

Effective March 1, 2026, TDI reduced promulgated title insurance rates by 6.2% following a rate hearing in December 2025. On a $450,000 purchase, the owner's policy premium dropped by approximately $145 under the new schedule. It's a modest saving, but it applies automatically to any transaction closing on or after March 1, 2026 — no action required on your part.

The only things that vary between title companies are the charges outside the promulgated premiums:

- Settlement or escrow fee

- Title search or exam fee

- Endorsement fees (e.g., survey deletion, lender-required endorsements)

- Overnight courier and miscellaneous fees

If you want to compare title companies, ask for a fee sheet and compare the non-promulgated charges.

Your Title Commitment — What to Look For Before Closing

Before closing, the title company will send you a Title Commitment — the document outlining what they will and won't insure. Most buyers glance at it and file it away. That's a mistake.

The commitment has three key schedules:

Schedule A — The basics: the effective date, who the policy covers, the coverage amounts, and the legal description of the property.

Schedule B-I — Requirements. These are conditions the title company needs to satisfy before they'll issue the policy — things like paying off the seller's existing mortgage, releasing any liens, or clearing a judgment. You want to see this list shrink to zero by closing day.

Schedule B-II — Exceptions. This is the list of items the policy won't cover. It will almost always include recorded easements (utility lines, drainage easements, access rights), deed restrictions in the subdivision, and any matters a new survey would reveal.

The Schedule B-II exceptions aren't necessarily a problem — most of them are standard and expected. But there are a few things worth flagging:

- Any easements that affect how you can use the property or where you can build

- Any encroachments or boundary issues noted in a prior survey

- HOA restrictions that might affect your renovation plans

- Any outstanding judgment liens not listed in Schedule B-I requirements

Ask your agent to walk you through the commitment before closing. If something in Schedule B-II catches your attention, bring it up during the option period — that's the right time to ask questions, not the morning of closing.

One note on surveys in Texas: if you obtain a new survey and your title company issues a survey deletion endorsement, they'll agree to remove certain survey-related exceptions from Schedule B-II. This provides stronger coverage and is generally worth the added cost on older properties or homes with complicated lot configurations. Your agent can advise on whether it makes sense for your specific purchase.

If you're buying in Fate, Royse City, Lavon, or other newer development areas, also ask about any MUD or PID district notices that may appear on your title commitment — these affect your property taxes and are worth understanding before you close. We covered those in detail in our post on MUD and PID taxes in the eastern DFW growth zones.

And one more thing worth mentioning: wire fraud is a real and increasing risk in Texas real estate closings. Before wiring your closing funds, call the title company directly using a phone number you find independently — not from an email. Verify the wire instructions by phone before sending a single dollar. Email-based wire fraud has cost Texas buyers tens of thousands of dollars in recent years.

Title insurance doesn't cover wire fraud losses, because the theft happens after closing — not through a defect in the title itself. Your vigilance at this step protects you where the policy cannot.

Frequently Asked Questions

Who pays for title insurance in Texas?

By custom in most Texas counties — including Rockwall and Dallas — the seller pays for the Owner's Policy (T-1) and the buyer pays for the Lender's Policy (T-2). Both are negotiable in the TREC contract. In a buyer's market, sellers sometimes agree to pay both policies as a concession.

What does title insurance cover for a buyer in Texas?

The Owner's Policy protects you against financial loss from title defects that existed before you purchased the property — including unpaid liens, forged documents, undisclosed heirs, and errors in public records. If any of these issues surface, the title company defends you in court and pays for covered losses up to the policy limit, for as long as you or your heirs own the home.

What is a title commitment and what should I look for?

A title commitment is delivered before closing and outlines what the title company will and won't insure. Schedule A covers what the policy protects. Schedule B-I lists requirements the title company needs satisfied before issuing the policy. Schedule B-II lists exceptions — items the policy won't cover, such as easements, deed restrictions, and any survey issues found in public records. Review Schedule B-II with your agent before closing, and raise any questions during the option period.

Did Texas title insurance rates change in 2026?

Yes. The Texas Department of Insurance reduced promulgated title insurance rates by 6.2% effective March 1, 2026. Since rates are set by TDI and the same at every title company in Texas, all buyers and sellers closing after March 1 benefit automatically. On a $400,000 purchase, the owner's policy dropped by approximately $145 under the new schedule.

Can I shop for a lower title insurance price in Texas?

You can't shop the T-1 or T-2 premium itself — those are set statewide by TDI and the same at every title company. What you can compare between companies is the settlement or escrow fee ($250–$750), title search fees, and endorsement costs. Ask any title company for a fee sheet to compare the non-promulgated charges.

Title insurance isn't the most exciting part of buying a home, but it's one of the protections you want in place and working correctly before you ever need it. The good news in Texas is that the system is straightforward — promulgated rates, a clear custom on who pays what, and a title commitment that shows you exactly what you're getting before you commit to closing.

If you're a buyer and your closing is coming up, take fifteen minutes to review the title commitment with your agent before signing day. If anything in Schedule B-II looks unfamiliar or raises a question, that conversation is much easier to have during the option period than at the closing table.

If you're still in the early stages of your search and want a clear picture of what to expect from first showing through closing, our free 90 Ways We Serve Buyers guide walks through every step The Dunnican Team handles — including the title and closing process — from start to finish.

About Cindy Dunnican

Cindy Dunnican is the managing partner of The Dunnican Team at Coldwell Banker Apex, Realtors, serving the Northeast Dallas suburbs, Rockwall County, and the surrounding North Texas communities. Alongside her husband and business partner, Cory, she helps buyers and sellers navigate move-up purchases, downsizing, relocation, new construction, and luxury lake and golf course properties. Connect with The Dunnican Team at thedunnicanteam.com.